1 INSTITUTO DE TURISMO DE ESPAÑA Antonio Nieto Magro Vocal asesor 24 de Septiembre de 2015...

29

1 INSTITUTO DE TURISMO DE ESPAÑA Antonio Nieto Magro Vocal asesor 24 de Septiembre de 2015 Seminario Islandia: Un mercado, un destino

Transcript of 1 INSTITUTO DE TURISMO DE ESPAÑA Antonio Nieto Magro Vocal asesor 24 de Septiembre de 2015...

1

INSTITUTODE TURISMO

DE ESPAÑA

Antonio Nieto Magro

Vocal asesor

24 de Septiembre de 2015

Seminario Islandia: Un mercado, un destino

2

Spill-over

effect on

economy

5.7% of world exports

9% of

employment

1,135Million

International tourists

15.3% of Spain exports

12.7% of

employment

65 millionInternational

tourists

Sources: Instituto Nacional de Estadística, UNWTO, World Economic Forum. 2013

WORLD

SPAIN

20.5% of Icelandexports

5.8% of

employment

1 millionInternational

tourists

ICELAND

1. Tourism contribution to economy World, Iceland and Spain

3

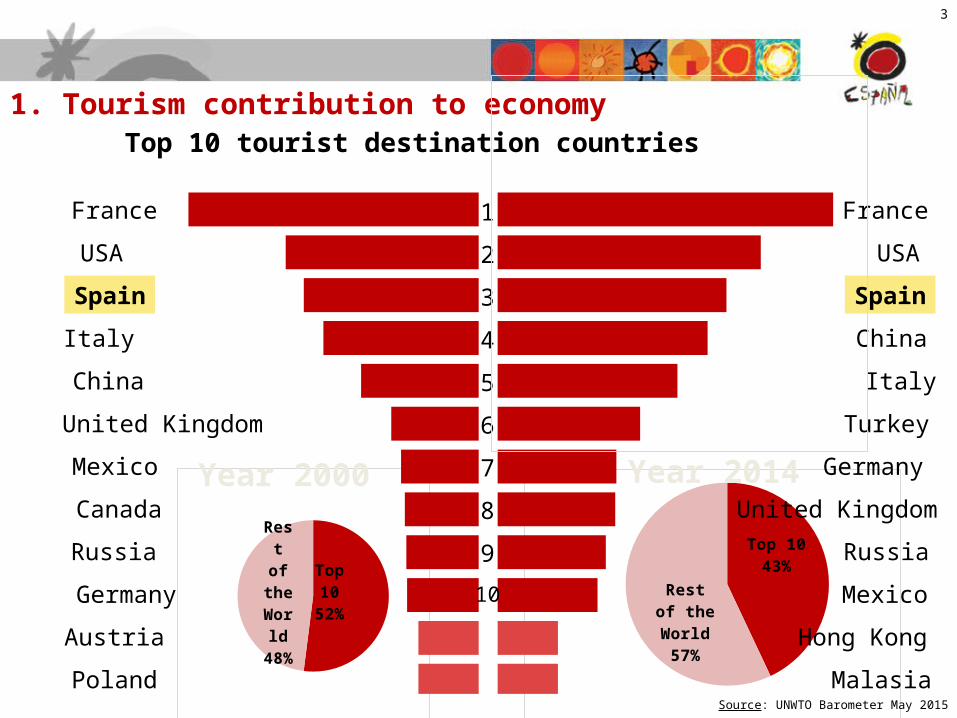

1. Tourism contribution to economy Top 10 tourist destination countries

Top 1043%

Rest of the

World57%

Top 10

52%

Rest of the World

48%

Source: UNWTO Barometer May 2015

USA

France France

USA

Spain Spain

Italy China

ItalyChina

United Kingdom

United Kingdom

Turkey

Mexico Germany

Canada

Russia

Mexico

Russia

Germany

Austria

Poland Malasia

Hong Kong

1

2

3

4

5

6

7

8

9

10

Year 2000 Year 2014

4

2. Tourism in Spain: Main facts and figures 2014

140 million trips by Spanish residents

within Spain en 2014 (-3%)

63.094 Mill. €

Total expenditurein 2014 (+6,5%).

Both average spending and average daily spending grew

65 million international

touristsin 2014 (+7%)

Spain is the third country in the world in terms of international arrivals, second in terms of travel receipts (UNWTO) and the first in terms of Tourist

Competitiveness (World Economic Forum)

35.389Mill. € surplus

Travel & Tourism Balance of Payments in 2014 (+1,9%)

165% of trade deficit

68 million international passengers

arrived at Spanish airports in 2014 (+6%)

48% with low cost carriers

(+10%)

295 million hotel overnights

in 2014 (+3%)

65% by non residents (+2,9%)

8

North America2,2% share

-0,3% decrease

Latin América

2,6% share+4,6% growth

Main European markets

86% share+7% growth

Rest of Europe

5% share+6,7% growth

Oceania0,4% share

-2,7% decrease

Asia2,9% share

+22% growth

Africa1%

share+18%

Source: TURESPAÑA. Frontur 2014

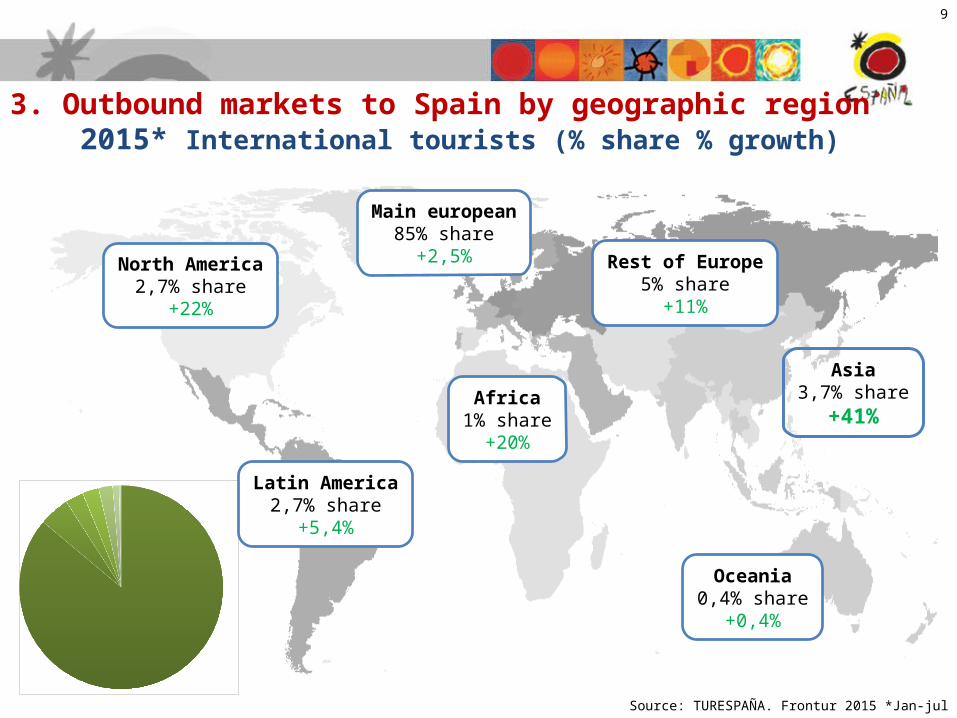

3. Outbound markets to Spain by geographic region 2014 International tourists (% share % growth)

9

North America

2,7% share+22%

Latin America

2,7% share+5,4%

Main european85% share

+2,5%Rest of Europe

5% share+11%

Oceania0,4% share+0,4%

Asia3,7% share+41%

Africa1%

share+20%

3. Outbound markets to Spain by geographic region 2015* International tourists (% share % growth)

Source: TURESPAÑA. Frontur 2015 *Jan-jul

10

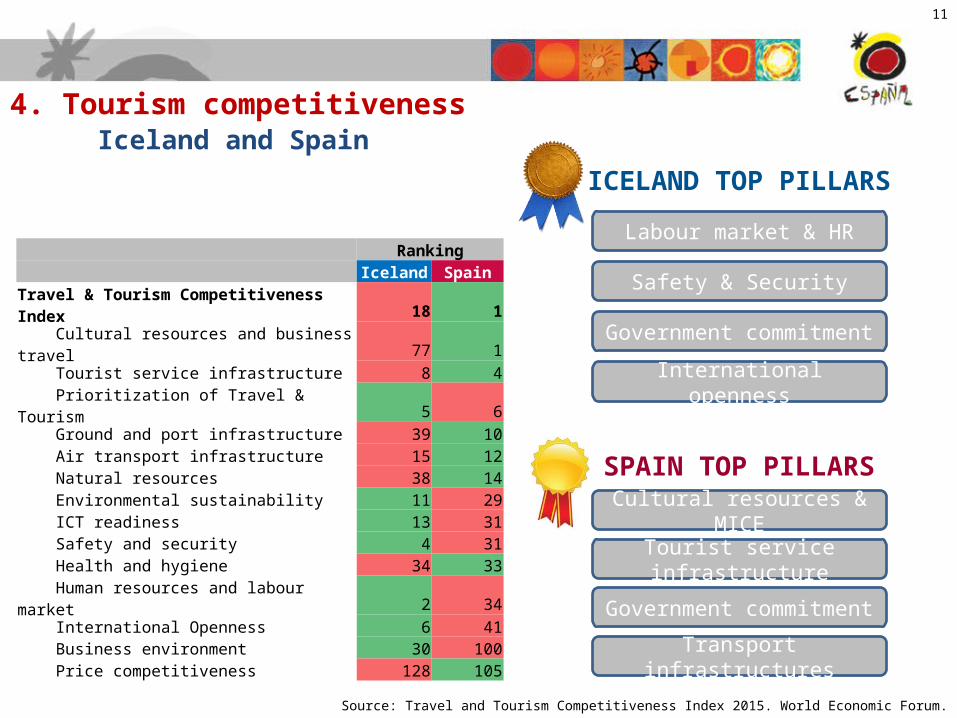

Source: Travel and Tourism Competitiveness Index 2015. World Economic Forum.

4. Tourism competitiveness World Economic Forum

11

Source: Travel and Tourism Competitiveness Index 2015. World Economic Forum.

4. Tourism competitiveness Iceland and Spain

Ranking Iceland SpainTravel & Tourism Competitiveness Index 18 1 Cultural resources and business travel 77 1 Tourist service infrastructure 8 4 Prioritization of Travel & Tourism 5 6 Ground and port infrastructure 39 10 Air transport infrastructure 15 12 Natural resources 38 14 Environmental sustainability 11 29 ICT readiness 13 31 Safety and security 4 31 Health and hygiene 34 33 Human resources and labour market 2 34 International Openness 6 41 Business environment 30 100 Price competitiveness 128 105

ICELAND TOP PILLARS

Labour market & HR

Safety & Security

Government commitment

International openness

Cultural resources & MICE

Tourist service infrastructure

Government commitment

Transport infrastructures

SPAIN TOP PILLARS

12

Source: UNWTO Basic indicators 2013

5. Comparative view of tourism sector in Iceland and Spain

Occupancy rate54.3%

Occupancy rate57,2%

Rooms906.289

Bed-places1,874.896

Bed-places23,738

Rooms11,422

Av. length of stay 2 days

Av. length of stay 3,4 days

ICELAND SPAIN

Hotels422

Hotels19.318

13

Spanish Constitution 1978

The Regions/Comunidades Autónomas “are responsible for the promotion and regulation of Tourism within their

geografic area.”

State competences:

• Plans to develope and promote tourist products

• International tourist cooperation.

• Cooperation with private sector .

• Relations with Comunidades Autónomas.

• General coordination of tourist activity.

• International promotion and commercialization support .

• Tourist Intelligence and Statistics.

7. Distribution of Tourism Competences in Spain Territorial coordination

14

7. Distribution of Tourism Competences in Spain Territorial coordination

Central

Administration

Autonomous & local

Administration

Private

entities

Interministerial Commission Departamentos ministeriales

Sectorial ConferenceAutonomous Regions

Council of TourismPrivate&public

Advisory Council of TourspainPrivate&Public – decision-making

about TourSpain’s activities

15

Transformations with important implications on Tourism

Socio-demográphic changes

Economic changes

Technologic changes

8. Tourism policy goals and objectives in Spain Global trends – effects on tourism. Huge changes

16

7 main goals :

• Grow tourist activity and profitability.

• Generate quality employment.

• Promote market unity and competitiveness.

• Improve international positioning.

• Improve awareness and cohesiveness of the brand Spain.

• Improve private-public partnership.

• Reduce seasonality.

This goals are facilitated mainly trough 3 means:

• Better knowledge, entrepreneurship and education.

• Updating tourist offer.

• Diversifying tourist demand.

8. Tourism policy goals and objectives in Spain Current tourism policy: National and Integral Tourism Plan 12-15 (PNIT)

17

BRANDING

Spain Brand

Strategic Marketing Plan

Permanent representation in

the UE

CLIENT ORIENTATION

Spain loyalty

Encourage national demand

New airport taxes

Optimise visa processing

SUPPLY & DESTINATIONS

Support to mature destinations’ restructuring

Credits to update infrastructures

Redefine

local small destinations

Intelligent destinations

Network of agencies

specialised in experiences

Homogenise classification

Developmetn of Spanish Tourism Quality System

Cultural, natural and gastronomic

heritage

Encourage Sustainable

tourism

ALIGNMENT

Analise the impact on tourism of new

regulations

Market unitiy

Changes in legislation

Private sector starts to have an

input on Tourspain’s

decision making

Support internationalisation

Cutting red tape

KNOWLEDGE

List of services

Modernise STOs

New orientation of Tourism Statistics

ENTREPENEURS

Monetary help for young

entrepeneurs

Tourism Entrepeneurs Programme

Adapt formative offer to market

demands

8. Tourism policy goals and objectives in Spain Current tourism policy: National and Integral Tourism Plan 12-15 (PNIT)

18

•Playa de Palma

•Costa del Sol Occidental

•San Bartolomé de Tirajana

•Puerto de la Cruz

Simulation Playa de Palma after

Playa de Palma Before

Total investment on 4 projects:

51,4 million euros

REQUALIFICATION OF MATURE DESTINATIONS

4 Projects

9. Main action areas Supply oriented activities

19

9. Main action areas Supply oriented activities

COMPETITIVENESS PLANS

Objectives:

Increase competitiveness, sustainability and

accessibility in tourist destinations.

Fight seasonality creating new products.

Promote high potential products.

Maximize commitment among administrations at

all levels: central, autonomous and local.

A total amount of 256 plans since 1993

20

205 local projects493 million euros

CREDIT LINES FOR LOCAL ENTITIES & BUSINESSES

9. Main action areas Supply oriented activities

FOMITMODERNIZATION OF TOURISM

INFRASTRUCTURES

EMPRENDETURINTERNACIONALIZATION

33 million euros in

2014 and 2015

21

9. Main action areas Supply oriented activities

What is a Product Club? • A strategic alliance among tourism managers, businesses, institutions to create and manage a

sustainable tourism product• A Set of well-structured tourist services• Guarantee for consumers• Association of businesses• A method of planification and promotion

Objective• Ensure the quality and sustainability of best products and promote them in an efficient manner

STRUCTURED PRODUCT CLUBS

Structure

Management

Planification

Private Busines

s

Administrations

Institutions

Promotion

&

Evaluation

22

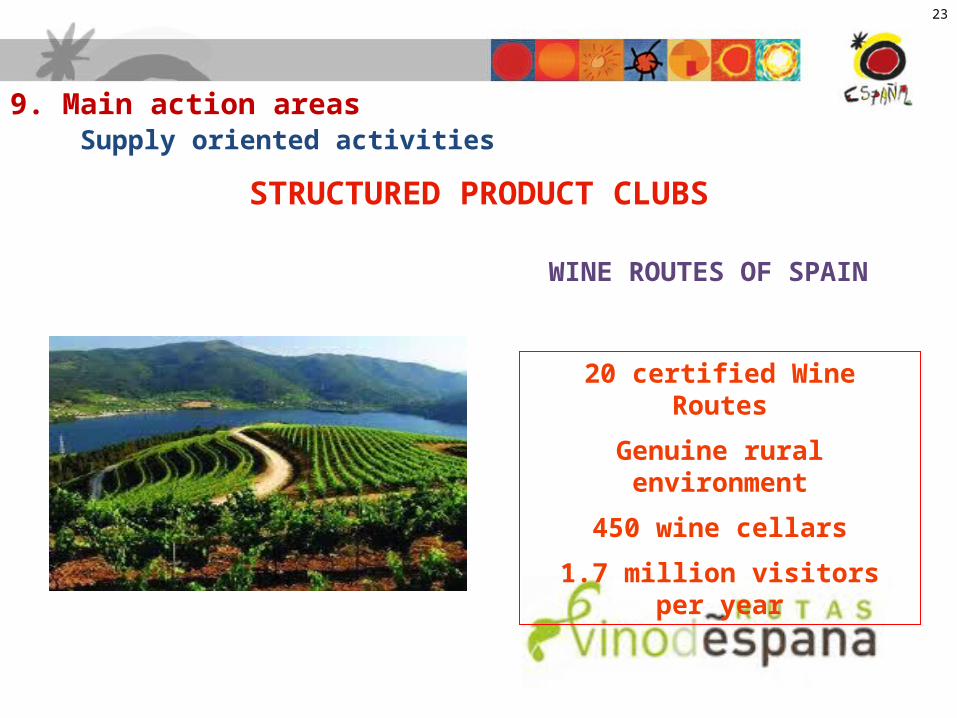

9. Main action areas Supply oriented activities

STRUCTURED PRODUCT CLUBS

ECOTURISM CLUB

47 UNESCO Biosphere reserves (2nd in the

world)

More than 400 businesses in Spain

attached

23

9. Main action areas Supply oriented activities

STRUCTURED PRODUCT CLUBS

WINE ROUTES OF SPAIN

20 certified Wine Routes

Genuine rural environment

450 wine cellars

1.7 million visitors per year

24

9. Main action areas Supply oriented activities

STRUCTURED PRODUCT CLUBS

ROUTE OF JAMÓN IBÉRICO

Genuine spanish gastronomy

5 destinations D.O. Jamón Ibérico

25

9. Main action areas Supply oriented activities

STRUCTURED PRODUCT CLUBS

HEALTH TOURISM: SPAIN CARES

Close cooperation between private and

public sector

Foster Spain promotion as Health and wellness

destination

50 hospitals 100 treatments inluded.

26

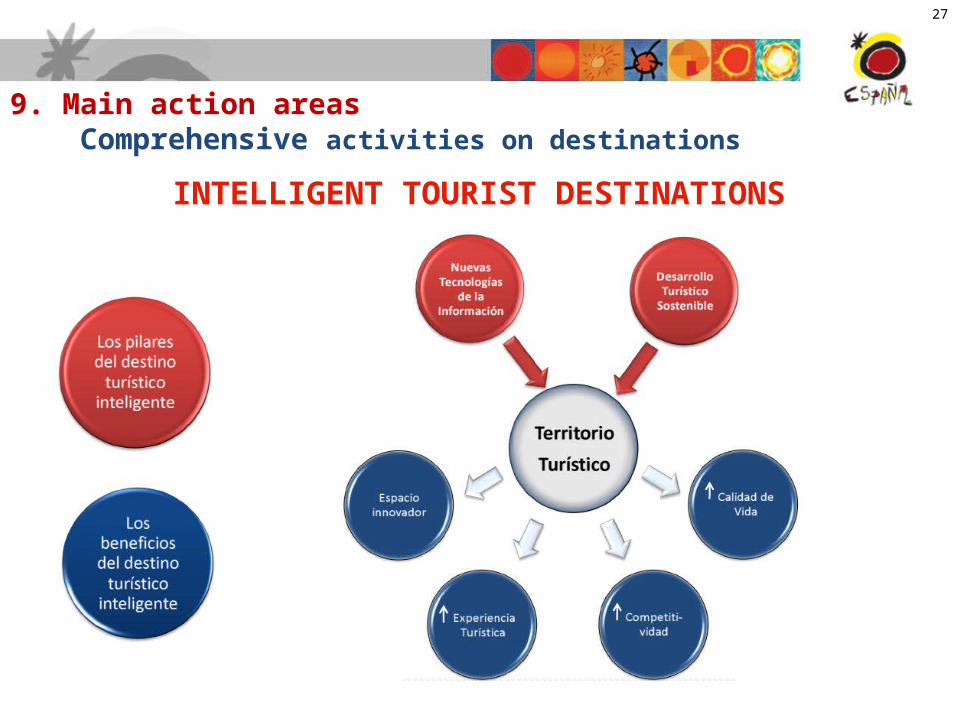

9. Main action areas Comprehensive activities on destinations

INTELLIGENT TOURIST DESTINATIONS

27

9. Main action areas Comprehensive activities on destinations

INTELLIGENT TOURIST DESTINATIONS

28

Demand research and market knowledge by TOS

STRATEGIC MARKETING PLAN

Strategic Marketing Plan 2012-2015

Global Plan

Regional Strategic Marketing Plans

Annual Tactical Plans

9. Main action areas Definition and execution of Spain’s marketing strategy abroad

29

RELAX DISCOVER ENJOY LEARN MEET

By the sea City breaks Night life Spanish MICE

In the countryside Itineraries Food and Wine Other courses

Campings Art & culture Shopping

Wellness Nature Special interest

Big Events Golf

Water sports

Adventure sports

Winter sports

Other sports

STRATEGIC MARKETING PLAN

9. Main action areas Definition and execution of Spain’s marketing strategy abroad

30

• Developing market intelligence.

• Positioning Spain’s image abroad

• Working together with opinion leaders, media and tour operators

• Supporting the marketing activities of Spanish destinations and companies

• Executing the Annual Marketing Plans in cooperation with the Autonomous Communities.

33 offices abroad, covering 79 markets

grouped in 8 regional areas

MORE THAN 60 YEARS AT THE SERVICE OF SPAIN’S TOURISM

9. Main action areas Definition and execution of Spain’s marketing strategy abroad

31

Annual Operative Plans (POA)Planification of activities for the whole 2015

3,000 annual activitiesTo promote spanish tourist destinations abroad

25,000 international travel agents

8,500journalists

1,800 fam and press trips for

3,000 professionals

2,000 press articles published

Advertising Value Equivalency

of 90 millon euros

45 millon consumers reached

50 millon impacts

9. Main action areas Definition and execution of Spain’s marketing strategy abroad

32

Thank you very much

INSTITUTODE TURISMO

DE ESPAÑA

Antonio Nieto Magro

www.tourspain.eswww.spain.info