Congreso Nacional de Minería...02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10...

24

Congreso Nacional de Minería Retos y Riesgos Globales de la Minería 2017 Mayo 10, 2017

Transcript of Congreso Nacional de Minería...02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10...

Congreso Nacionalde MineríaRetos y Riesgos Globales de la Minería 2017Mayo 10, 2017

Page 2

Mining sector globally … and locally!

“The only thing constant is volatility”MiningSector

GloballyIs not about Crisis … is about Volatility …

Page 3

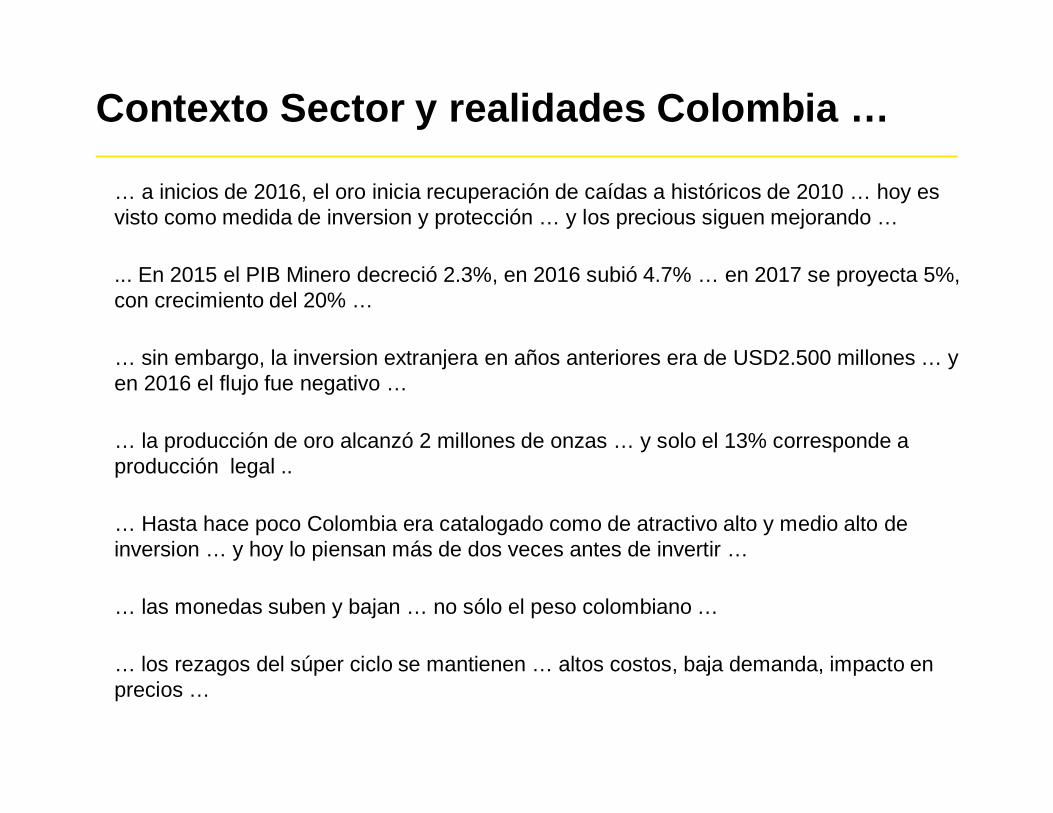

… a inicios de 2016, el oro inicia recuperación de caídas a históricos de 2010 … hoy esvisto como medida de inversion y protección … y los precious siguen mejorando …

... En 2015 el PIB Minero decreció 2.3%, en 2016 subió 4.7% … en 2017 se proyecta 5%,con crecimiento del 20% …

… sin embargo, la inversion extranjera en años anteriores era de USD2.500 millones … yen 2016 el flujo fue negativo …

… la producción de oro alcanzó 2 millones de onzas … y solo el 13% corresponde aproducción legal ..

… Hasta hace poco Colombia era catalogado como de atractivo alto y medio alto deinversion … y hoy lo piensan más de dos veces antes de invertir …

… las monedas suben y bajan … no sólo el peso colombiano …

… los rezagos del súper ciclo se mantienen … altos costos, baja demanda, impacto enprecios …

Contexto Sector y realidades Colombia …

Page 4

Retos y riesgos en Minería 2017Perspectiva EY

910

81

4

52

3

Resource nationalism

10

23

45

67

89

1

Up from 2015 Same as 2015Down from 2015 New to the radar

Page 5

Outlook en los últimos años…

Page 6

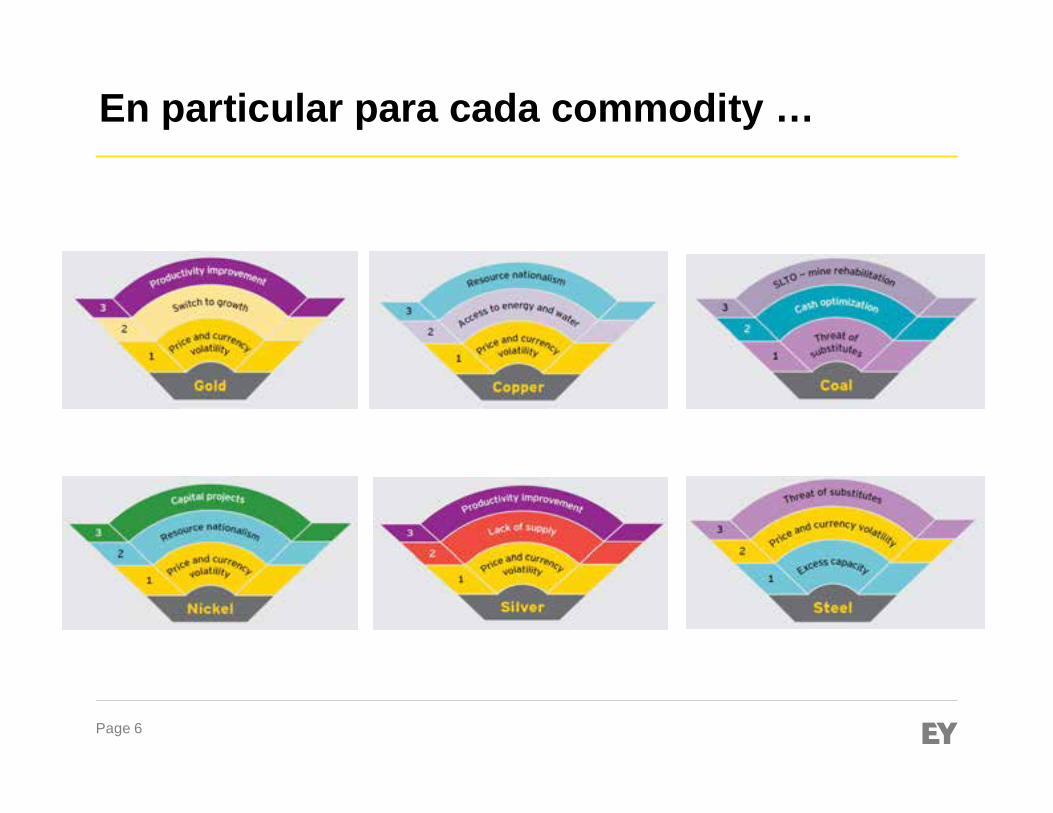

En particular para cada commodity …

Page 7

Retos y riesgos en Minería 2017Perspectiva EY

Percepción del Sector en Colombia*

* No exhaustivo, basado en conversaciones con Compañías, Instituciones yAcademia en Colombia, e interpretación de noticias de actualidad

Estudio Global EY

Factores críticos queimpactan la percepción:§ Incertidumbre jurídica§ Coordinación institucional§ Informalidad e ilegalidad§ Protestas y relaciones con la

comunidad§ Recursos especializados limitados§ Limitaciones logísticas, de

infraestructura y seguridad-

12

34

5

2017

Page 8

Ahora … hacia dónde se estánenfocando los esfuerzos a nivel globaly local para mitigar los impactos deesos retos y riesgos de sector?

Page 9

Cash optimizationIndustry margins are hit by a number of factors

Volatility in mineralprices

AusterityHigh Costs of ProductionComponents

Margin Squeeze

(manpower, assets,processes and logistics)

Poor capital projectexecution

Devaluation inproducer currencies

Lack of costcontainment discipline

Wrong perception of thereal mining situation

Cash Optimization

“2017 is about switch to growth … the austerity mode can leave us behind …”Top 10 mining companies

Page 10

Source: Australian Bureau ofStatistics

40

60

80

100

120

140

16019

94-9

5

1995

-96

1996

-97

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

Market sectors (ex. mining) index Mining productivity index

Mining labor productivity has declined by roughly 50% since 200319

94–

95

1195

–96

1996

–97

1997

–19

98

2000

–20

01

2001

–20

02

2002

–20

03

2003

–20

04

2004

–20

05

2005

–20

06

2006

–20

07

2007

–20

08

2008

–20

09

2009

–20

10

2010

–20

11

2011

–20

12

2012

–20

13

2013

–20

14

2014

–20

15

ProductivitySystematic end-to-end transformation

Page 11

What companies are doing …

During super cycle,productivity fell to its lowestrate in more than 30 years …

► Tax efficient supply chain

► Inbound logistics review

► Operational Improvement

► Operational efficiency in labour,equipment and technology

► Strategic sourcing

► Inter-productive Value Chains► Capability Modelling► Mining scenario modelling► Transportation network optimisation► Internet of the things and Advanced

Data Analytics► Product recovery model

Procurement and sourcing fromenterprise intelligence

Page 12

► Building a strong platform for continuous business improvement and growth … notfocus in baseline risks, but incorporating the holistic risk radar …

What companies are doing …Strengthening the Risk Management perspective

§ Productivity andEfficiency

§ Processes and Controls

§ Data and InformationManagement

§ Organizational structureand capabilities

§ Technology andOperational tools

§ Responsible Mining

§ Regulatory compliance

§ Responsible supply chainand human rights

§ Labor rights and workconditions

§ Business Partners andThird Parties

Page 13

Local case:► Informality and Illegal Operations► Community Protests► Competition between extraction and

traditional production activities► Potential environmental impacts due to

close operations on water sources

Response:► Focus on relationships with all stakeholders► Inter-productive value chains with

community► Active and visible Formalization Programs► Pro-activity with planning so prepared to

deal with new issues

“Social concerns about impacts are beginning to lead to increased regulation”

Top 10 mining company

Localcommunities

NGOs &Activists Employees

SuppliersInvestorsCustomers

DigitalCommunities

RegulatorybodiesGovernments

Social license to operate

Page 14

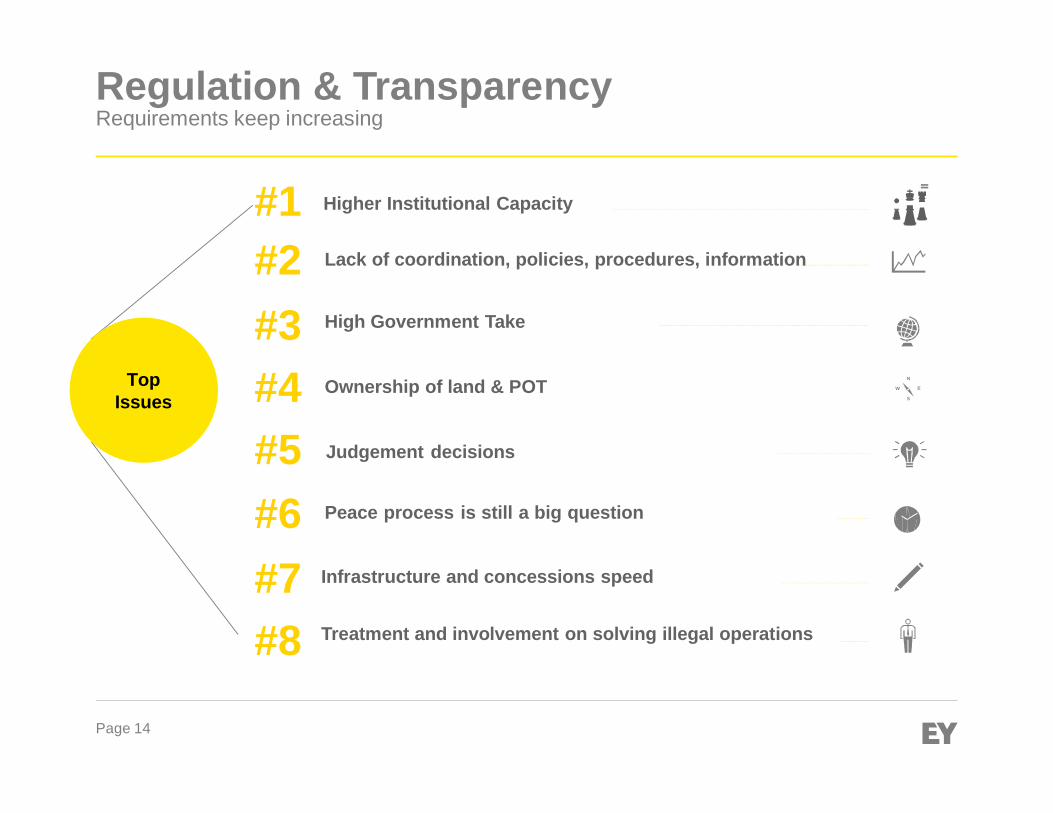

Regulation & TransparencyRequirements keep increasing

#1#2#3#4#5#6#7#8

Higher Institutional Capacity

Lack of coordination, policies, procedures, information

N

High Government Take

W E

S

Peace process is still a big question

Infrastructure and concessions speed

Ownership of land & POT

Judgement decisions

Treatment and involvement on solving illegal operations

TopIssues

Page 15

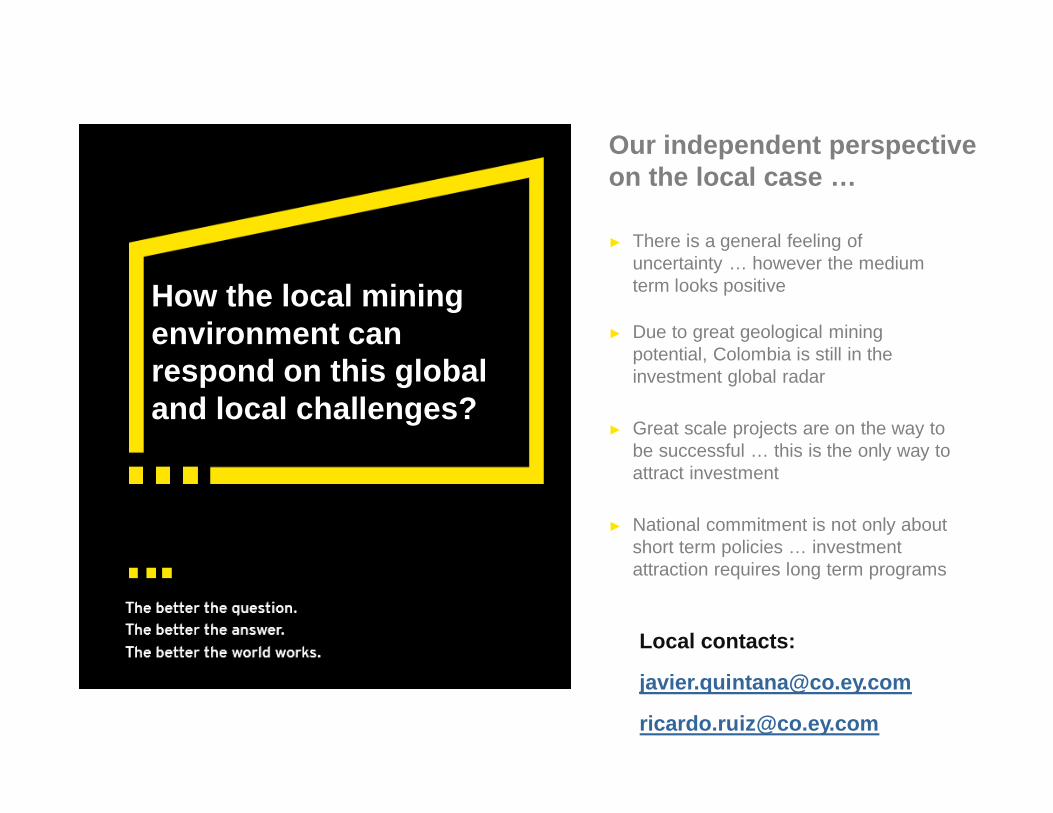

How the local miningenvironment canrespond on this globaland local challenges?

Our independent perspectiveon the local case …

► There is a general feeling ofuncertainty … however the mediumterm looks positive

► Due to great geological miningpotential, Colombia is still in theinvestment global radar

► Great scale projects are on the way tobe successful … this is the only way toattract investment

► National commitment is not only aboutshort term policies … investmentattraction requires long term programs

Local contacts:

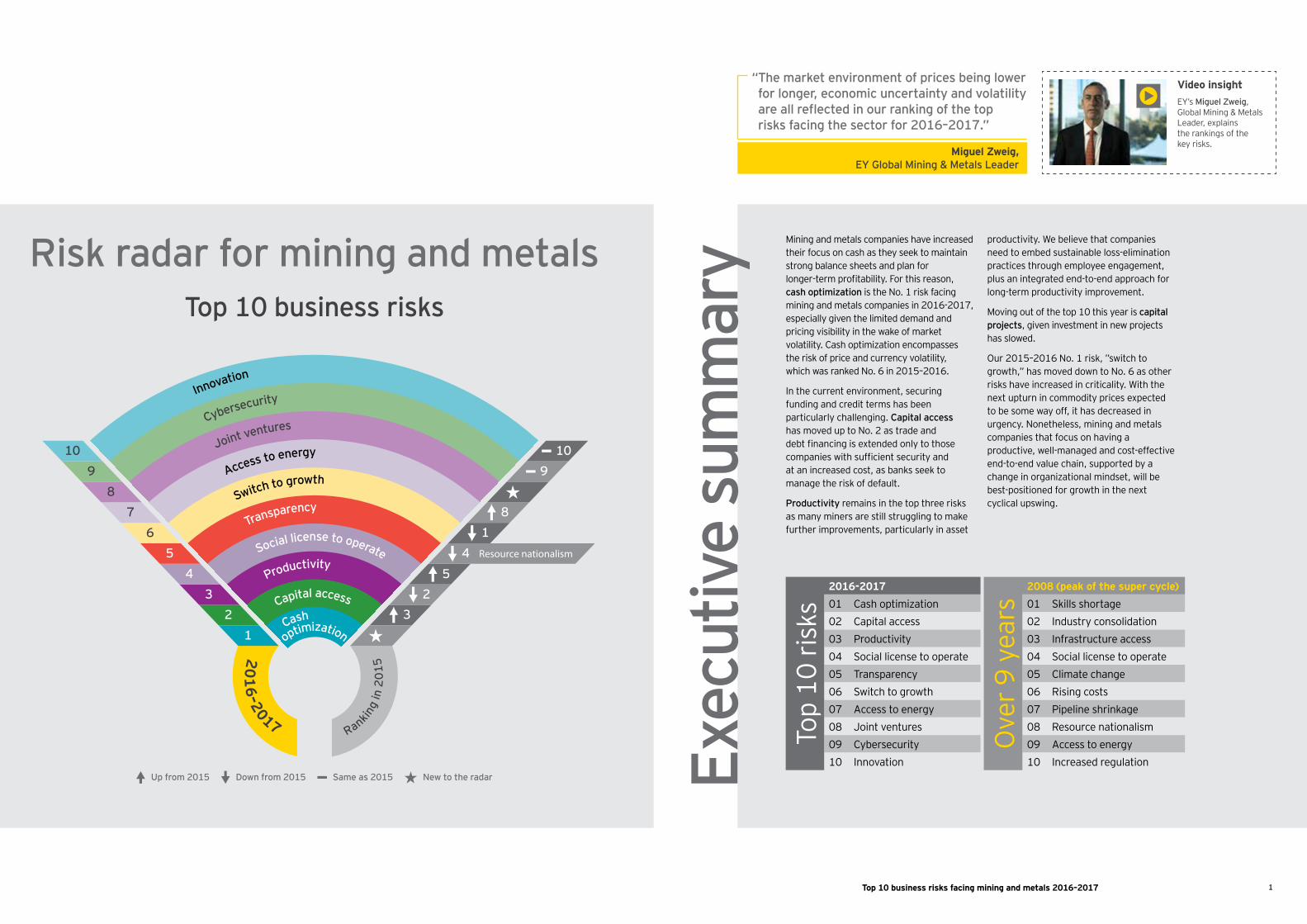

Top 10 business risks facing mining and metals, 2016–2017

1T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 7

Top 10 business risk s

Risk radar for m ining and m etals

10

12

34

56

78

9

Resource nationalism

910

81

45

23

Rank ing

in 2

015

U p from 20 15 S am e as 20 15D ow n from 20 15 N ew to the radar

201

6 – 2 0 1 7

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation

Exec

utiv

e su

mm

ary

“ The m ark et environm ent of p rices being low er for longer, econom ic uncertainty and volatility are all reflected in our ranking of the top risk s facing the sector for 20 16 – 20 17 . ”

M ig ue l Z w e ig , E Y G lobal M ining & M etals L eader

M ining and metals companies have increased their focus on cash as they seek to maintain strong balance sheets and plan for lon e te p ofitability o t i ea on cash op tim iz ation i t e o i acin

inin and etal co panie in especially given the limited demand and pricing visibility in the w ake of market olatility a opti i ation enco pa e

t e i o p ice and c ency olatility ic a an ed o in

n t e c ent en i on ent ec in funding and credit terms has been pa tic la ly c allen in C ap ital access

a o ed p to o a t ade and debt financin i e tended only to t o e co panie it ficient ec ity and at an inc ea ed co t a ban ee to

ana e t e i o de a lt

Productivity remains in the top three risks as many miners are still struggling to make

t e i p o e ent pa tic la ly in a et

p od cti ity e belie e t at co panie need to embed sustainable loss-elimination p actice t o e ployee en a e ent plus an integrated end-to-end approach for lon te p od cti ity i p o e ent

o in o t o t e top t i yea i cap ital p roj ects i en in e t ent in ne p o ect

a lo ed

o i itc to o t a o ed do n to o a ot e

i a e inc ea ed in c iticality it t e ne t pt n in co odity p ice e pected to be o e ay o it a dec ea ed in

ency onet ele inin and etal companies that focus on having a p od cti e ell ana ed and co t e ecti e end to end al e c ain ppo ted by a c an e in o ani ational ind et ill be be t po itioned o o t in t e ne t cyclical p in

op

i

2 0 1 6 - 2 0 1 7

Ove

r 9 y

ears

2 0 0 8 ( p e ak o f t h e s up e r c y c l e )a opti i ation Skills shortage

0 2 apital acce 0 2 I ndustry consolidation0 3 P roductivity 0 3 I nfrastructure access0 4 Social license to operate 0 4 Social license to operate

T ransparency li ate c an eSw itch to grow th R ising costsA ccess to energy P ipeline shrinkage

0 8 J oint ventures 0 8 R esource nationalism0 9 ybe ec ity 0 9 A ccess to energy

I nnovation I ncreased regulation

E Y ’s M iguel Z w eig G lobal M ining & M etals

eade e plain the rankings of the ey i

V id e o ins ig h t

3T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 7T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 72

0 2C ash op tim iz ation

C ap ital access

10

12

34

56

78

9

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation1C ash

op tim iz ation

10

12

34

56

78

9

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation2

C ap ital access

C ash generation and p reservation w ill rem ain a k ey focus for the m edium term due to ongoing m ark et volatility.

W ith lim ited access to cap ital, com p anies are look ing at alternative sources of finance and portfolio realignment options.

K e y t h o ug h t K e y t h o ug h t

(N ew ) o in

L im ited p ricing and dem and visibility as a result of ongoing m ark et volatility is challenging m ining and m etals com p anies as they p lan for the future. C ash is k ing once again as com p anies seek to m aintain balance sheet liq uidity and im p lem ent p lans to boost operational cash flow for long-term profitability.

C ap ital raising continues to be an issue in the sector. I n 20 15 , cap ital raised w as dow n by about 10 % Y O Y . There w as a sharp decline in loan finance to the sector, and m ost loans w ere used for refinancing existing facilities rather than going into new p roj ects.

e t e pa t ont a t e i o de a lt a inc ea ed ban a e only e tendin t ade and lon te financin at an increased cost to those mining and

etal co panie it ficient ec ity to bac t e debt n an a y bot c edit de a lt ap p ead and yield pea ed it c edit acce e ainin con t ained ince

inin co panie lobally i analy i show ed that many miners had still not actively focused on w orking capital as a le e to i p o e ca o ed ce co t and i p o e a e olde et n a in an ente p i e led app oac co bined w ith a bottom-up change management p o a a elea ed ca o totalin ten o billion o dolla i en t at the aggregate levels of w orking capital in the sector amount to more than

b t e e a e till plenty o oppo t nitie to t e elea e ca

• I m p rove cap ital effectiveness: t actin o e al e o e i tin a et p e ent

an opportunity to improve asset ana e ent capability i can elp to

drive productivity and manage risk in a co t con t ained en i on ent o e ey areas w here w e believe improvements can be identified incl de a i t o calendar- to condition-based maintenance w ith appropriate overall eq uipment e ficiency et ic p io iti in sustaining capital and taking a top-dow n approach to facilitate appropriate capital allocation and e ecti e cont ol o i

e e pect t e co t o capital to e ain ele ated in nle t e co odity p icin en i on ent i p o e o po ate credit ratings continue to be placed on either ne ati e atc o do n aded ile ban e ain a y o e tendin c edit to t e ecto ity a et in t alia anada

and t e a e li ely to e ain bd ed w ith the potential risk of shareholder dilution

o place ent o i t i e p o pted by financial di t e

i ate e ity and ell capitali ed producers continue to look for opportunities in t e ecto e e entitie a e li ely to e ain electi e on deployin capital

ta etin lo co t de i ed ope ation it o tp t eadily a etable to end e

T heir subseq uent risk appetite w ill dete ine t e ini et n needed w ith interest potentially skew ed tow ard lon li e a et in ope ation o ca ce t ate ically i po tant ind t ial ine al

n o ie t e e a e t ee ey oc a ea by w hich mining and metals companies can effectively manage liq uidity:

• M ak e sustainable cost reductions that do not erode value: in t e inin boo co t e calated b tantially in o e ca e by oon a p ice ta ted declinin ine too ea e to lo e their costs and protect their margins by traditional means such as headcount ed ction and ot ballin p o ect o e e a p ice loo li e t ey ill be

lo e o lon e ine need to ta e a lon e te o e tainable app oac to ana in t ei co t nde tandin

at co t ed ction need to be ade o ic ly t ey can be i ple ented

w hat the payback period is and how long t ey can be tained i ey o panie need to act now to protect margins and ed ce e po e to c ent and t e

co t inc ea e e a e al eady een mining and metals companies being in enti e in t e a ea o co t ed ction o e a ple by c allen in all a ea o

e pen e incl din t e need o t a el considering the offshore sourcing of standard components and consolidating suppliers to facilitate a more effective ne otiation on p ice

• I ncrease focus on w ork ing cap ital: I n our ecent epo t Making working capital

work for you: unlocking cash in the mining sector e analy ed t e o in capital performance of 8 0 of the largest

T he backdrop of challenging market conditions has led to a number of alternative financin t ate ie bein p ed e e

e e a o t ea in deal in o t b p o b t o yea

ea lie n il e eaton anno nced U S$ 9 4 0 m w orth of precious metal streams

ile anco e ada i ned on o a il e and old t ea o

lenco e ntapaccay ine in e e e have also been a large number of royalty a ee ent o ta e and o a d ale a

ell a a et bac ed financin on in ento y and t ade ecei able

o panie a e al o loo in at t ei po t olio ic ay lead to di e t ent of non-core assets or offering minority po ition to oint ent e pa tne to ed ce cape e i e ent and aintain

ope ational e ibility i enable financial ead oo to cope it olatility and con ince lende o t e iability

o ce o on analy i

4 0 0

Proc

eeds

(US$

b)

3 5 03 0 02 5 02 0 01 5 01 0 0

5 00

2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 Q 1 5 2 Q 1 6

Num

ber o

f iss

ues

3 , 5 0 0

3 , 0 0 0

2 , 5 0 0

2 , 0 0 0

1 , 5 0 0

1 , 0 0 0

5 0 0

0

T otal volumeD ebtE q uity

0 1Capital raised — value and volume (2011–2Q16)

e da ide o etal t ea in deal t apped inin co panie t ade t e al e o ca Financial Post ece be

V id e o ins ig h t

E Y ’s L ee D ow nham lobal inin etal an action eade

di c e capital opti i ation in inin and etal and t e ey i e to con ide

V id e o ins ig h t

E Y ’s L ee D ow nham lobal inin etal an action eade

discusses capital access in mining and metals and t e ey i e to con ide

5T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 7T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 74

0 4Productivity S ocial license

to op erate

10

12

34

56

78

9

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation

3Productivity

10

12

34

56

78

9

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation

4

S ocial license to op erate

Productivity rem ains the p rim ary op erational challenge in the m ining sector, w ith m any still struggling to m ak e an im p act.

M ining and m etals com p anies need to em bed sustainability into long- term p lanning and op erate in tandem w ith local com m unities to retain social license to op erate ( S L TO ) .

K e y t h o ug h t K e y t h o ug h t

o in o in

I n E Y ’ s p ap er, Productivity in mining: now comes the hard part, we identified that the focus on “ volum e at any cost” during the boom generated a focus on grow th and m eant m ines had to be larger. S caling up these structures m ade them m ore com p lex to run and resulted in silos and dim inished connectivity w ithin op erations. I t created an integration gap w ithin businesses, and dealing w ith it req uires an end- to- end ap p roach.

M ine accidents, m ining- related diseases, com m unity p rotests and neglecting m ine rehabilitation obligations are all having a significant impact on the sector’ s im age and, in turn, on the ability of the com p anies to retain their S L TO . The follow ing are a few of such recent im p acts: • e a e ob e ed a all i e in atal

accident in ai in t e ollo in q uestions: I s cost-cutting undermining the oc on e o a 3 e tec nolo y

systems and safety being adeq uately e o ced to be e ecti e e co panie

at risk of undoing some of the successes in ac ie in bette a ety c lt e

P roduction uptime can q uickly be increased by p to and e en e en ance ent can typically be deli e ed in t e an e o

it o t i nificant in e t ent o table and p edictable ope ation

p od cti ity pa tic la ly a o nd ope ation and aintenance acti itie can al o be inc ea ed pe ation pendin le ti e dealing w ith emergencies can create opportunities to support continuous i p o e ent e o t a e lt t i app oac t an late into i p o ed a ety better forecasting and advanced inte ated acti ity plannin

T he critical role that people can play in the productivity transformation cannot be

nde e ti ated od cti ity i p o e ent i the responsibility of everyone in the o ani ation elentle p it o lo li e e o a can t an o t e b ine i ible leade ip and i nificant in e t ent

in culture change and capability are critical to eac t e ne t le el o p od cti ity

ban ptcy e tion a e bein ai ed a to w ho w ill pick up the cost of mine clo e and e abilitatin ine ite

co panie do not ana e t i i e t en o e n ent ill a e to tep in o e a ple in een land t alia a

chain-of-responsibility legislation w as p opo ed in a c to p e ent ta paye o a in to pay o en i on ental clean p

o aintain a t on it i i po tant to integrate sustainability into long-term planning and link key performance indicators w ith productivity outcomes as

ell a e ne ation t ct e cce l companies have highlighted the value of operating in tandem w ith communities and have show n that it is possible to engage t o t al al e c eation o e a ple o e in o e local o ne ip and sourcing labor and procurement domestically w ill provide a greater le el o co nity en a e ent

ac pa t o t e b ine o ld be opti i ed not on its ow n but as part of a business y te e belie e t at t e inin ecto

can learn a lot from other sectors on how to do t i e e i e idence o i nificant productivity improvement and value creation through the adoption of a manufacturing

ind et e eby t e e i a elentle oc on the elimination of loss across the o ani ation octe a ble o e a ple is a leader in this space through its integrated

o y te ic a enabled t e co pany to ac ie e a in o b o e t e pa t t ee yea 2 T here is also a move tow ard di itali ation o t e al e c ain a o e companies are implementing information systems to manage the full value stream using real-time production reporting systems

ile al o ad tin t ei ana e ent ope atin y te to be o e data o iented

e e co panie a e i ple ented action to o e to a d ope ational eliability i nificant benefit a e been ac ie ed

• M ining-related diseases such as silicosis and pneumoconiosis (black lung disease) a e bac in oc n t e fi t confi ed ca e o blac l n di ea e in yea a epo ted in t alia 4 R esurgence of these diseases means that mining companies w ill face increased e lato y acti ity ne and ti te d t

li it ope ational c an e and inc ea ed co po ate liability e a e al eady ob e ed la e cale ealt elated ci il clai o e a ple in ay a o t ican i o t led t at people w ho contracted silicosis and T B as a result of unsafe conditions at mines co ld oin to et e in a cla action law suit against mining companies for co pen ation

• T he crippling costs of mine rehabilitation are making it tough to seal deals on pits eac in t e end o t ei ine li e e e

t an action a e been co pleted ne ow ners are often continuing to produce e en at a lo in o e ca e to a oid

clo e co t n addition a inin companies go into administration or

o pply ain an o ation a ed illion GT Nexus website acce ed ay

o a ety no pain Australasian Mine Safety Journal ctobe acce ed ne

lac n di ea e t e leepin iant a in p Clayton Utz insights ay acce ed ne

ll ine o e in o t ica in i to ic ilico i battle The Economist, ay

onfidence in t e inin ind t y e ollo in le i lation in een land Mining Global ay acce ed ne

The key to achieving long-term sustainable productivity improvement

Focus on the assets, end-to-end view

Relentless pursuit of loss

Support your people

0 3

1 2 3

V id e o ins ig h t

E Y ’s Paul M itchell lobal inin etal d i o y eade

discusses the importance of productivity in mining and the key issues miners need to con ide

http://www.ey.com/GL/en/Industries/Mining---Metals/EY-productivity-in-mining-now-comes-the-hard-part

http://www.ey.com/GL/en/Industries/Mining---Metals/EY-productivity-in-mining-now-comes-the-hard-part

7T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 7T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 76

0 6Transp arency S w itch to

grow th

10

12

34

56

78

9

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation

5

Transp arency

10

12

34

56

78

9

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation

6

S w itch to grow th

W hile resource nationalism has slow ed, transp arency initiatives are accelerating.

S w itching to grow th at the right tim e to tak e advantage of a buyer’ s m ark et w ill boost long- term shareholder value.

K e y t h o ug h t K e y t h o ug h t

o in o in

W hile resource nationalism has retreated in m any regions over the p ast 12 m onths, transp arency initiatives continue to gain m om entum as governm ents seek to im p rove governance in their countries.

M ining and m etals com p anies need to break free of the p ro-cyclical, short- term behavior that currently p revails. E ven though it now ap p ears that com m odity p rices w ill be low er for longer, p rep aring for future grow th rem ains essential if com p anies are to stay ahead of the com p etition. A clear understanding of grow th op tions available — w hether to build or buy — is essential. This req uires an ongoing aw areness of the m ark et ( cap ital m ark ets, global sup p ly and dem and, geop olitical develop m ents and custom er behavior) and the com p etition. I t m ay also involve a p rocess of dow nsiz ing ex isting p ortfolios to realiz e cap ital and free up scarce resources to sup p ort future grow th op p ortunities.

ltiple tanda d ail e to do o ill att act penaltie o nonco pliance and in o e ca e ay a e c i inal con e ence a e lt companies need to:

• I dentify the level and granularity of disclosure and reporting necessary and then establish processes to gather and assemble the data regarding government payments for proper reporting

• e ie t ei y te to confi t at they have captured the detail and data as req uired

• onfi t at t e data i eliable and tell the story that they are happy to share publicly

T he reporting of government payments is and ill e ain a i nificant c allen e o

any b t can only elp to en ance in e to confidence and ene ate t t it ta e olde it io into epo tin on

it ta e ince in an ann al Taxes Paid p blication ot e la e lobal inin companies have also started to voluntarily di clo e t ei o e n ent pay ent

M anaging liq uidity must be balanced w ith asset portfolios that represent attractive

a e olde al e t o t e ole cycle A lthough companies have focused on reducing cash outlays and increasing financial e ibility belie e t at continued volatility represents an opportunity to reposition portfolios for a cyclical eco e y

denti yin a ea o o t in con nction w ith near-term liq uidity should remain an i po tant con ide ation o ana e ent especially w hen planning to create

a e olde al e i al o incl de di ital strategy and cultivating the right skills and people i i an opti ti e to t in about the diversity and skills needed for the

t e oin o ay acilitate t e ti ely acq uisition of assets that could otherw ise be di fic lt to ec e a te a ll cyclical eco e y t al o elp in a oidin t e al e de t ction o payin e ce i e

acq uisition premiums and in beating competitors by opportunistically securing t e t on e t a et a ead o t e a et

oc on t an pa ency at e t an on e o ce nationali in t n i p o e

the investment climate of a country by providing a clear signal to investors and inte national financial in tit tion t at t e government is committed to good

o e nance and le o la p o in transparency can help mining and metals co panie o t ei ocial cont ib tion providing local communities w ith greater acce to in o ation and in t n helping to refute claims of not paying t ei ai a e

I nitiatives to promote transparency started it t e t acti e nd t ie an pa ency

nitiati e in i a ollo ed by any ot e co nt y and e ion pecific di clo e initiati e in t e t e and

anada o e detail abo t t e e lin can be found in E Y ’s paper Disclosing payments to governments in an era of transparency

T hese initiatives affect all mining and etal co panie e a dle o e e t ey

ope ate it o e a in to co ply it

e fi t al o itne ed e e al opportunistic acq uisitions aimed at gaining e po e to pecific etal i p o in

a etin p e i eali in ope atin yne ie o addin cale to e i tin

ope ation ne c e a ple i a ic old di e t ent o ald

M ountain and R ound M ountain to K inross old o p to t en t en it po t olio and elp lo e t e co pany co t p ofile eyond i p o in e e e li e and lfillin t ate ic ob ecti e t e e t an action

t e pple ent e i tin co t c ttin initiatives by being value-accretive to ta e olde in t e o t te i i

probably the best time for mid-tiers w ith ood financial bac in to ac i e i

ality a et a t e a o e oc t ei po t olio and ell t e a et t at do not fit t ei co e b ine ina olybden o in tance a ta en ad anta e o t e

c ent a et en i on ent pendin b on tie ac i ition in

o n lo e ican and eepo t c o an d i in pec lation t at it ay

beco e a lobal inin a o t o ac i ition 8

in o ac i e t ate ic e ada a et Kinross Gold Corporation press release o e be

ina olybden till in a et o tie a et SNL ne

R e s o urc e nat io nal is m up d at e sY ou can access the latest resource nationalism q uarterly updates in E Y ’sMining & Metals Quarterly Briefing

0 5

9T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 7T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 78

0 8A ccess to energy

J oint ventures

10

12

34

56

78

9

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation

7

A ccess to energy 10

12

34

56

78

9

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation

8

J oint ventures

I t is no longer a m atter of scarcity, but rather the ability to identify, p rioritiz e and im p lem ent the best source of energy for long-term tangible and intangible benefits.

W hile there is a great up side to j oint ventures ( J V s) , the risk s to non- op erators is significant given their lack of inclusion in op erational decisions w hich can have large k nock - on effects.

K e y t h o ug h t K e y t h o ug h t

o in (N ew )

A s energy consum p tion can be anyw here from 15 % to 4 0 % of the op erating budget of a m ine, cost is naturally an im p ortant consideration w hen choosing an ap p rop riate source of energy. H ow ever, this is only one asp ect of a far larger strategic decision. O ther considerations are:• U ncertainty of availability and cost of

energy over the entire mine life• o nte pa ty i• Operational alternatives • ocial financial and ep tational

implications of every choiceM ining and metals companies today often use a i o ene y o ce typically a co bination o o il el yd oelect icity and ene able ene y a yin by location ene y pplie and capital a ailability i en the rapidly increasing competitiveness of ene able ene y ind ene y and ola

ene y in pa tic la la e ene y con e a e nde ta in a i nificant c an e in o they procure and generate the energy they need ene able ene y can p o ide t e

C om p anies enter into J V arrangem ents for a variety of reasons, including cap ital intensity, risk m itigation, access to resources and technology, sup p ly chain op tim iz ation, m ark et p ositioning, regulatory req uirem ents or p olitical sensitivities.

n addition to t e co t a in t e deci ion to adopt renew able sources of energy and reduce energy consumption is also being in enced by national and e ional policie and le i lation to ed ce ca bon e i ion

e e al ine incl din io into and n lo e ican a e i ned t e a i led e o

ction at in ppo t o t e a ee ent to limit the global w arming temperature rise to le t an de ee el i io into focuses on technological development to i p o e ene y ol tion o e a ple it a

ode ni ed it iti at al in elte t o t e e o ene y e ficient tec nolo y ic a i p o ed t e ene y inten ity o t e elte by

I f the energy consumer is w illing to enter into an appropriate long-term pow er purchase a ee ent o t e elect icity it con e renew able energy plants can be independently de eloped b ilt financed and ope ated o t at t e e benefit a e loc ed in o t e con e it ope atin a in

being so dependent on both commodity p ice and ene y p ice inc ea ed oc on renew able energy and smarter energy solutions by the mining and metals co nity i li ely to contin e

nd e ac en ie o illiton brought J V s into stark focus w hen he said that the group w as looking into w hether governance should change at non-operated

e aid t at illiton o ld ee et e a o e pet ole type odel

i t be o e app op iate in t e t e o it non ope ated inin ent e

N on-operating J V partners need to consider w hat mitigation strategies should be put in place to p otect t ei in e t ent c a conducting non-operator audits or embedding non-operator management to p o ide inc ea ed i ibility e la challenges by active investors w ill remove complacency and demand a greater consideration of all stakeholder interests

en a in ope ational deci ion

it lon te fi ed p ice elect icity t iti atin any e po e to el p ice olatility

in t e t e be it oil and a p ice o t e cost of importing electricity from neighboring co nt ie ene able ene y ill al o ed ce e po e to any di ect o indi ect poll tant co t c a een o e a e o ca bon ta e ene able ene y can al o e lt in di ect financial benefit by t e a ailin o local incenti e capital allo ance o ed ced t an i ion co t n a et c a o t

ica and ile ene able ene y plant a e currently generating electricity at a cheaper price than anything provided by local utilities and at a p ice i nificantly c eape t an any on ite die el ene ation

n ite ene able ene y ene ation e ficiency tec nolo ie and ic o id a e helping mining and metals companies to c eate i nificant ope ational co t a in T he use of combined storage and P V hybrid systems9 can halve the fuel costs of off-grid producers that are currently reliant on liq uid fossil fuels being transported and consumed on ite i i in addition to financial ocial and ep tational benefit t at ay acc e due to reducing diesel-related greenhouse

a e i ion and poll tant

en a e ana ed ell t ey a e the potential to deliver substantial value to ta e olde i nificantly en ancin t e

value of company portfolios and access to e e e and capabilitie o e e en

t e e elation ip o on t ey can be e t e ely di pti e pa tic la ly to p o ect c ed le and ey deci ion point ide o t e di ption to t e co e b ine

arbitration and legal proceedings relating to any failure can be costly and time-consuming distractions for the management o bot t e and t e pa ent o ani ation

N on-operators may be particularly vulnerable to operating risks as they have very limited say in the day-to-day operations at ine ite ny deci ion by t e ope ato could diminish value creation for the non-operator or even result in large penalties or liabilities in the event of accidents or other ope ational i e n t e la t e yea ope ational i a e beco e o co ple and dynamic that it is almost impossible for an operator or a non-operator to reasonably acto in i at t e ta t o a p o ect

illiton p t oint ent e nde e ie a te da b eac Financial Times o e be

ne y to a e yb id y te o e e potential o o id inin ecto pv-magazine a c acce ed ne

alancin ene y need and en i on ental i pact Rio Tinto website acce ed ly

0 7

11T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 7T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 710

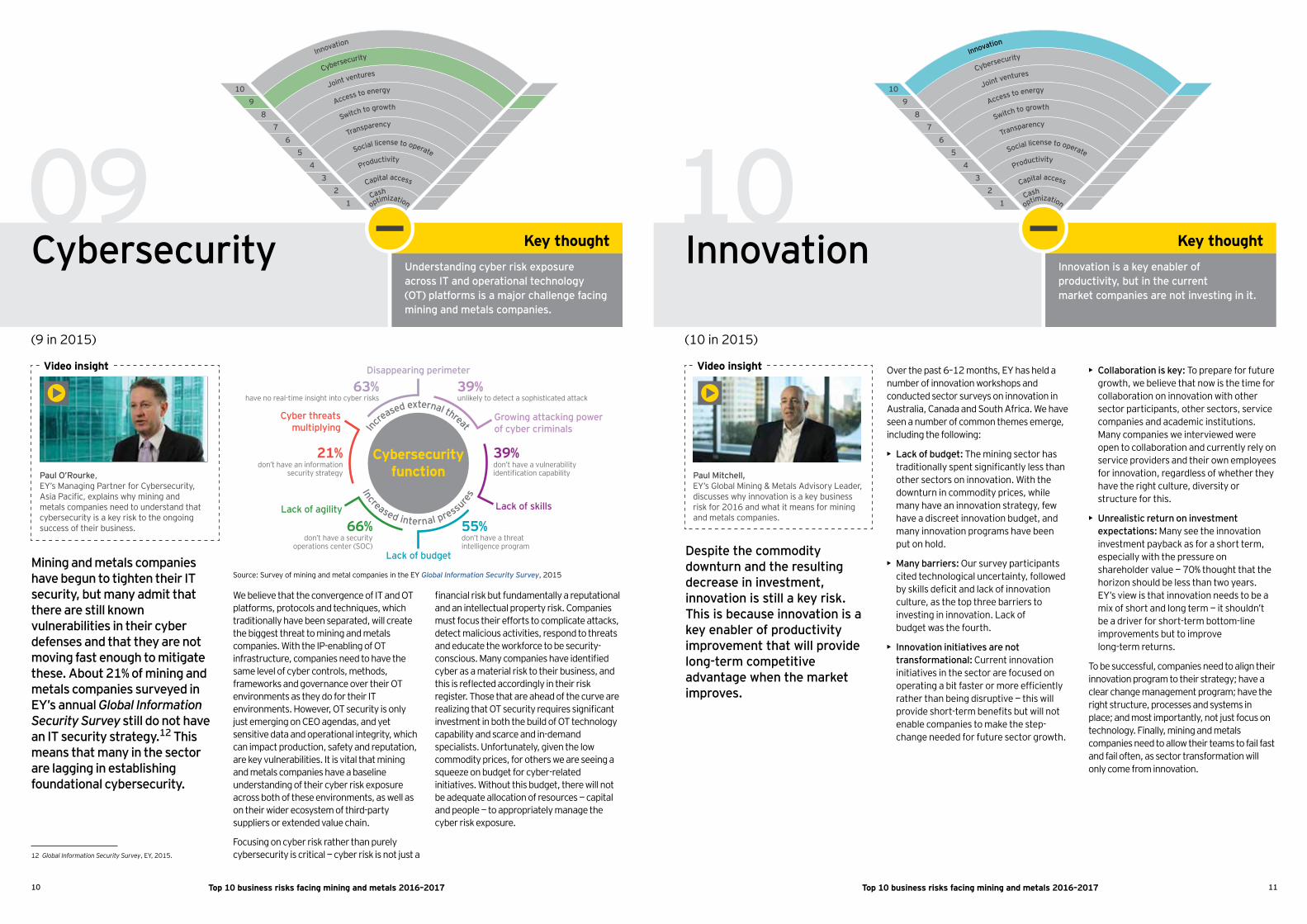

0 9 10C ybersecurity I nnovation

10

12

34

56

78

9

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation

C ybersecurity

910

12

34

56

78

9

C ybersecurity

A ccess to energy

S w itch to grow th

Transp arency

S ocial license to op erate

Productivity

C ap ital access

I nnovation

J oint ventures

C ash

op tim iz ation

10

I nnovation

U nderstanding cyber risk ex p osure across I T and op erational technology ( O T) p latform s is a m aj or challenge facing m ining and m etals com p anies.

I nnovation is a k ey enabler of p roductivity, but in the current m ark et com p anies are not investing in it.

K e y t h o ug h t K e y t h o ug h t

in in

M ining and m etals com p anies have begun to tighten their I T security, but m any adm it that there are still k now n vulnerabilities in their cyber defenses and that they are not m oving fast enough to m itigate these. A bout 21% of m ining and m etals com p anies surveyed in E Y ’ s annual Global Information Security Survey still do not have an I T security strategy. 12 This m eans that m any in the sector are lagging in establishing foundational cybersecurity.

D esp ite the com m odity dow nturn and the resulting decrease in investm ent, innovation is still a k ey risk . This is because innovation is a k ey enabler of p roductivity im p rovem ent that w ill p rovide long- term com p etitive advantage w hen the m ark et im p roves.

financial i b t nda entally a ep tational and an intellect al p ope ty i o panie

t oc t ei e o t to co plicate attac detect alicio acti itie e pond to t eat and educate the w orkforce to be security-con cio any co panie a e identified cybe a a ate ial i to t ei b ine and t i i e ected acco din ly in t ei i e i te o e t at a e a ead o t e c e a e eali in t at ec ity e i e i nificant

investment in both the build of OT technology capability and scarce and in-demand peciali t n o t nately i en t e lo

co odity p ice o ot e e a e eein a ee e on b d et o cybe elated

initiati e it o t t i b d et t e e ill not be ade ate allocation o e o ce capital and people to app op iately ana e t e cybe i e po e

• C ollaboration is k ey: T o prepare for future o t e belie e t at no i t e ti e o

collaboration on innovation w ith other ecto pa ticipant ot e ecto e ice

co panie and acade ic in tit tion M any companies w e interview ed w ere open to collaboration and currently rely on service providers and their ow n employees o inno ation e a dle o et e t ey a e t e i t c lt e di e ity o t ct e o t i

• U nrealistic return on investm ent ex p ectations: M any see the innovation in e t ent paybac a o a o t te especially w ith the pressure on

a e olde al e t o t t at t e o i on o ld be le t an t o yea

E Y ’s view is that innovation needs to be a i o o t and lon te it o ldn t

be a driver for short-term bottom-line improvements but to improve lon te et n

o be cce l co panie need to ali n t ei innovation program to their strategy; have a clear change management program; have the i t t ct e p oce e and y te in

place and o t i po tantly not t oc on tec nolo y inally inin and etal companies need to allow their teams to fail fast and ail o ten a ecto t an o ation ill only co e o inno ation

e belie e t at t e con e ence o and plat o p otocol and tec ni e ic t aditionally a e been epa ated ill c eate the biggest threat to mining and metals co panie it t e enablin o in a t ct e co panie need to a e t e a e le el o cybe cont ol et od

framew orks and governance over their OT environments as they do for their I T en i on ent o e e ec ity i only

t e e in on a enda and yet en iti e data and ope ational inte ity ic

can i pact p od ction a ety and ep tation a e ey lne abilitie t i ital t at inin and metals companies have a baseline

nde tandin o t ei cybe i e po e ac o bot o t e e en i on ent a ell a on their w ider ecosystem of third-party

pplie o e tended al e c ain

oc in on cybe i at e t an p ely cybe ec ity i c itical cybe i i not t a

e t e pa t ont a eld a number of innovation w orkshops and conducted sector surveys on innovation in

t alia anada and o t ica e a e een a n be o co on t e e e e e

including the follow ing:

• L ack of budget: T he mining sector has t aditionally pent i nificantly le t an ot e ecto on inno ation it t e do nt n in co odity p ice ile

any a e an inno ation t ate y e a e a di c eet inno ation b d et and

many innovation programs have been p t on old

• M any barriers: Our survey participants cited tec nolo ical nce tainty ollo ed by ill deficit and lac o inno ation c lt e a t e top t ee ba ie to in e tin in inno ation ac o b d et a t e o t

• I nnovation initiatives are not transform ational: ent inno ation initiatives in the sector are focused on ope atin a bit a te o o e e ficiently at e t an bein di pti e t i ill

p o ide o t te benefit b t ill not enable companies to make the step-c an e needed o t e ecto o t

Global Information Security Survey

C y b e rs e c urit yf unc t io n

have no real-time insight into cyber risks6 3 %

don’t have an information security strategy

2 1 %

don’t have a security operations center (SOC)

6 6 %

D isap p earing p erim eter

unlikely to detect a sophisticated attack3 9 %

don’t have a vulnerability identification capability

3 9 %

don’t have a threat intelligence program

5 5 %

C yber threatsm ultip lying

L ack of agility

L ack of budget

L ack of sk ills

G row ing attack ing p ow erof cyber crim inals

I ncreased internal p ressu

res

I ncreased ex ternal threat

Source: Survey of mining and metal companies in the E Y Global Information Security Survey

V id e o ins ig h t

Paul O ’ Rourk e ana in a tne o ybe ec ity

ia acific e plain y inin and metals companies need to understand that cybersecurity is a key risk to the ongoing

cce o t ei b ine

V id e o ins ig h t

Paul M itchell, lobal inin etal d i o y eade

discusses w hy innovation is a key business i o and at it ean o inin

and etal co panie

1

2

3 Pip eline shrink age

Price and currency volatility

L e ad / z inc

S w itch to grow th

T o p ris k s f o r c o mmo d it ie s

S ustainingcap ital

1

2

3Productivity im p rovem ent

A ccess to energy

A l uminium

Threat of substitutes1

2

3 C ash op tim iz ation

S L TO — m ine rehabilitation

C o al

Price and currency volatility1

2

3A ccess to energy and w ater

Resource nationalism

C o p p e r

Price and currency volatility1

2

3 S w itch to grow th

Productivity im p rovem ent

G o l d

Productivity

p roductivity)1

2

3Price and currency volatility

C ap ital allocation

I ro n o re

( p articularly asset 1

2

3 Resource nationalism

C ap ital p roj ects

N ic k e l

Price and currency volatility1

2

3Productivity im p rovem ent

S L TO

P G M

Price and currencyvolatility

1

2

3 C ap ital p roj ects

Productivity im p rovem ent

P o t as h

Price and currency volatility1

2

3 L ack of sup p ly

Productivity im p rovem ent

S il v e r

Price and currency volatility1

2

3Price and currency volatility

Threat of substitutes

S t e e l

E x cess cap acity 1

2

3Price and currency volatility

Rising regulation

Uranium

Threat ofsubstitutes

13T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 7T o p 1 0 b us ine s s ris k s f ac ing mining and me t al s 2 0 1 6 – 2 0 1 712

N ote: ice and c ency olatility enco pa e t e top t o b ine i o ca opti i ation and capital acce

A bout E Y i a lobal leade in a ance ta t an action and ad i o y

e ice e in i t and ality e ice e deli e elp b ild t t and con idence in t e capital a et and in econo ie t e o ld o e

e de elop o t tandin leade o tea to deli e on o p o i e to all o o ta e olde n o doin e play a c itical ole in b ildin a bette o in o ld o o people o o client and o o co nitie

e e to t e lobal o ani ation and ay e e to one o o e o t e e be i o n t o n lobal i ited eac o ic i a epa ate le al entity n t o n lobal i ited a co pany li ited by a antee doe not p o ide e ice to client o o e in o ation abo t o o ani ation plea e i it ey co

i itedll i t e e ed

no

ency

one

T his material has been prepared for general informational purposes only and is not intended to be elied pon a acco ntin ta o ot e p o e ional ad ice lea e e e to yo ad i o o peci ic ad ice

ey. com / m iningm etals

E Y ance a an action d i o yHow EY’s Global Mining & Metals Network can help your business

it a olatile o tloo o t e ecto t e lobal inin and etal ind t y i oc ed on o to aintain a t on and e ible balance

eet ile p epa in o t e o t e ecto i al o aced it t e inc ea ed c allen e o i p o in p od cti ity acce to capital dealin it inc ea ed t an pa ency aintainin licen e to ope ate and cybe ec ity

E Y ’s G lobal M ining & M etals N etw ork is w here people and ideas come together to help mining and metals companies meet the issues of today and anticipate those of tomorrow by developing solutions to

eet t e e c allen e t b in to et e a o ld ide tea o p o e ional to elp yo cceed a tea it deep tec nical e pe ience in p o idin a ance ta t an action and ad i o y e ice to t e inin and etal ecto lti ately it enable to elp yo eet yo oal and co pete o e e ecti ely

E Y G lobal M ining & M etals L eaderM iguel Z w eigel i el ei b ey co

O ceaniaScott G rimleyel cott i ley a ey co

C hina and M ongoliaP eter M arkeyel

pete a ey cn ey co

J ap annd e o ell

el co ell nd inni on o p

A fricaic ot a

el ic bot a a ey co

C om m onw ealth of I ndep endent S tatesB oris Y atsenkoel

bo i yat en o ey co

F rance, L ux em burg, M aghreb, M E N A

i tian ionel

c i tian ion ey co

I ndian ani a al

el an ani a a al in ey co

U nited K ingdom & I relandee o n ael

ldo n a ey co

C anadaB ruce Spragueel

b ce p a e ca ey co

B raz ilA fonso Sartorioel

a on o a to io b ey co

C hilea a a ie a ont e a

el a ia a ie a cont e a cl ey co

Service line contacts

E Y G lobal A dvisory L eaderP aul M itchellel

pa l itc ell a ey co

E Y G lobal A ssurance L eaderle ei ano

el ale ei i ano ey co

E Y G lobal I F RS L eaderacey a in

el t acey a in a ey co

E Y G lobal Tax L eadernd e an inte

el and e an dinte a ey co

E Y G lobal Transactions L eaderee o n ael

ldo n a ey co

EY area contacts